By Stuarts Accountants

•

May 25, 2026

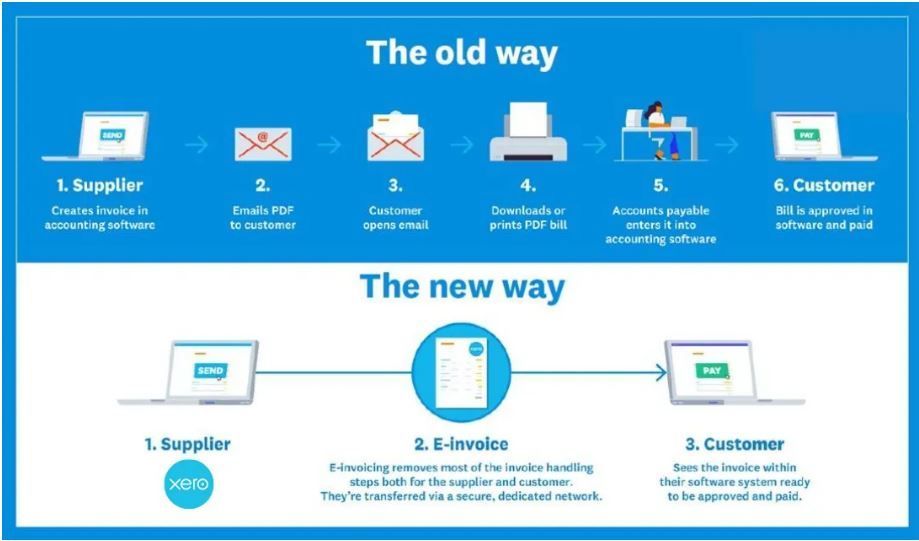

Over 50,000 Kiwi businesses are now set up for eInvoicing. What is eInvoicing? eInvoicing allows you to send and receive invoices electronically, directly to and from Xero, for faster payments, improved accuracy, and less manual data entry. Invoices arrive securely via Peppol, a global public network that has been endorsed by the New Zealand Government for electronic invoicing processing. STEP 1: Get registered To register email admin@stuarts.co.nz your business’s New Zealand Business Number (NZBN) and the details of the contact person you will nominate for your business. We will then complete your registration. Once registered, your business name, NZBN, country of registration and a unique participant ID will be publicly available through the Peppol directory. STEP 2: Get ready to send Before you start eInvoicing, your customer records need to include the New Zealand Business Number (NZBN) of the businesses you’ll be billing. Updating these details takes a little bit of setup now, for easier, safer invoicing ‘ever after’. It should only take a minute or two per customer, and there’s no need to update all your customer records at once – you can work through them one by one as it suits you. If you don’t have their NZBN, you can ask the customer, search on the NZBN directory, or use the free Business Match service on the NZBN website. If an organisation uses more than one NZBN across its business, select the one most relevant to you. In Xero: Contacts > Select Customer > Contact Details > Edit Contact > NZBN You'll also need to make sure your NZBN is in your organisation details: Account > Settings > Organisation Details > NZBN And if you're registered for GST, make sure your GST number is included in your financial settings: Account > Settings > Organisation Details > Advanced Settings > Financial Settings > GST Number And now you are ready to notify your customers! Because the more customers you send to, and receive from, the more benefit you’ll get. Smoother processing. Less errors and delays, allowing for faster payment. And, improved e-security. So encourage your buyers to eInvoice you - and give them the details they need. You can email your customers - but also update your email signatures, cost estimates, or other assets your customers frequently see. STEP 3: Receiving & Sending Once you’re registered for eInvoicing - you’re all ready to receive. Incoming eInvoices will appear as ‘Draft Bills’ in Xero - not via email - so if you don’t already check your draft bills regularly, it might be worth setting a reminder to do so. To send an eInvoice, just create an invoice as normal. Once you have entered the relevant contact, the option to ‘Send as an eInvoice’ will activate in the bottom right corner of the invoice screen. Once you select this option, complete the details of your invoice as normal. If your customer requires a purchase order, contract number, project number or tender number as part of an invoice, make sure this information is entered in the ‘Reference’ field.